Workers’ compensation insurance provides crucial protection for businesses and employees, covering salary, medical expenses, and legal fees in the event of workplace injuries. However, employers can further enhance their coverage through dividend plans, which allow policyholders to receive a percentage of their premium payments back at the end of the policy period.

Understanding Workers’ Comp Dividends

When choosing a workers’ compensation policy, many employers consider dividend plans as a way to save on premium costs. Like other workers’ comp policies, dividend plans cover medical expenses and lost wages to injured workers. However, with a dividend plan, qualifying employers can share in the profitability of the policy with the insurance company.

While premium rates are based on future trends, dividends are calculated using past performance. Essentially, they reward employers who maintain low loss ratios and have fewer claims.

Types of Dividend Plans

The two most common types of workers’ compensation dividend plans are flat and sliding scale; combination plans may also be available.

Flat

Under a flat dividend plan, eligible policyholders receive a specified percentage of their premium for the policy period, regardless of their loss experience. The typical amount is 5% or 10% of the premium. While poor loss experience won’t impact their dividend that period, it may disqualify them from enrolling in the plan for the next policy year.

Sliding-Scale

With a sliding-scale dividend plan, the amount of the dividend depends on the policyholder’s loss ratio. A lower loss ratio at the expiration date means a higher dividend payment, providing greater incentives for safety and risk management.

Combination

Less common combination plans incorporate elements of both flat and sliding scale plans. They may offer varying dividend percentages based on different premium thresholds, while also specifying a maximum loss ratio. If the loss ratio exceeds the maximum, no dividend is paid

Benefits for Employers:

Participating employers can garner several advantages through workers’ comp dividend plans

- Premium Savings: Employers save on premium costs for each claim dollar avoided, reducing their overall expenses for workers’ comp coverage.

- Safety Promotion: Dividend plans create a financial incentive for employers to prioritize safety in the workplace, leading to improved risk management practices and reduced injuries.

- No Penalty for Claims: Dividends can only reduce the policy price, ensuring that employers face no penalties for excessive or large claims, apart from not qualifying for the dividend.

- Significant Returns: Depending on the individual company’s policy, dividends can range from 10% up to 40%, representing a substantial financial benefit for employers.

Considerations and Limitations

Employers should keep the following points in mind when considering workers’ compensation dividend plans:

- Carrier Availability: Not all insurance companies offer dividend plans. Employers should research and select a carrier that provides this option before committing to coverage.

- Non-Guaranteed Dividends: Insurers cannot guarantee the payment of dividends. The decision to pay or withhold a dividend rests with the insurer’s board of directors and may be influenced by the company’s financial performance.

Although dividends are not guaranteed, these plans can incentivize business owners to implement workplace safety programs that mitigate the costs and risks associated with work-related injuries.

The Kinetic Dividend Program

Employers that choose a dividend plan and remain committed to promoting safety in the workplace can reduce their workers’ compensation costs and enjoy financial returns at the end of each policy period. Kinetic’s dividend program enables policyholders to recover up to 26% of their policy’s premium based on annual incurred losses.

And to help employers maximize their dividend return, Kinetic provides policyholders with free wearable technology proven to reduce sprain and strain injuries by over 50%.

Who’s Eligible?

Any Kinetic workers’ comp policyholder can access the dividend plan by meeting the following conditions:

- Policyholder agrees to deploy Kinetic’s injury-reducing wearable technology to some percentage of at-risk employees within four weeks of the policy effective date

- Policy premium meets the annual minimum threshold of $100,000, not including taxes and fees

- The incurred loss ratio at the time of the snapshot(s) is less than 40%

When Does the Program Payout?

Kinetic’s dividend pays out in two parts:

6 Months After Expiration

- The account has no open claims: 100% payout

- The account has outstanding open claims: 50% payout based on current loss ratio and premium range

18 Months After Expiration

- Unchanged loss ratio: 50% balance payout based on current claims

- Improved loss ratio: Revised payout applying the new loss ratio

- Degraded loss ratio beyond eligible range: No additional payout

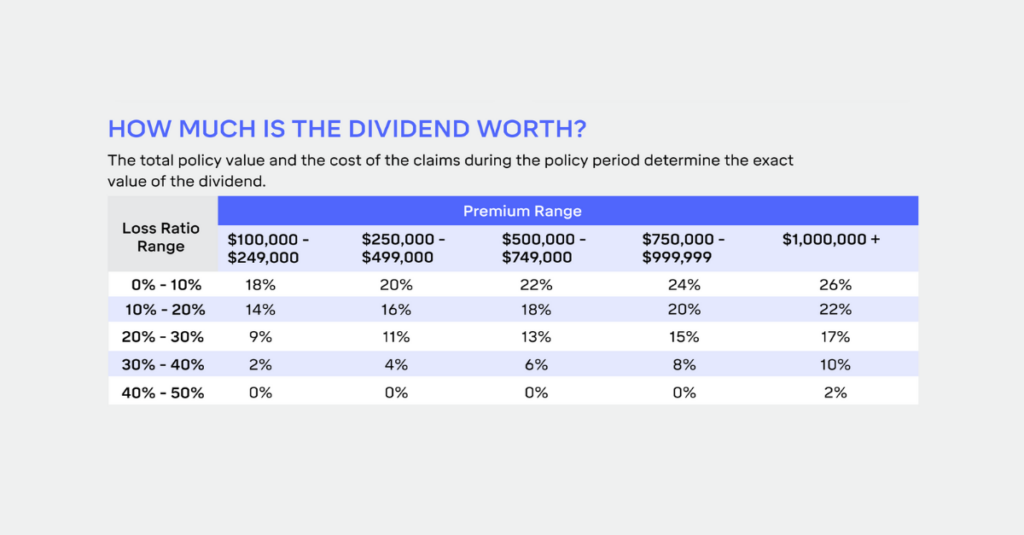

How Much is the Dividend Worth?

The total policy value and the cost of the claims during the policy period determine the exact value of the Kinetic dividend.

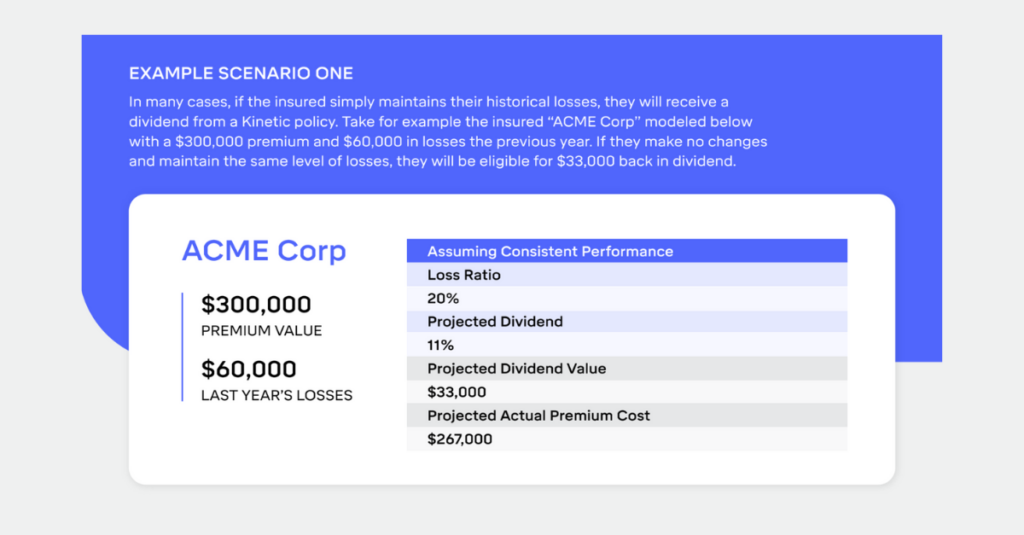

Example Scenario One

In many cases, if the insured simply maintains their historical losses, they will receive a dividend from a Kinetic policy. Take, for example, the insured “ACME Corp” modeled below with a $300,000 premium and $60,000 in losses the previous year. If they make no changes and maintain the same level of losses, they will be eligible for $33,000.

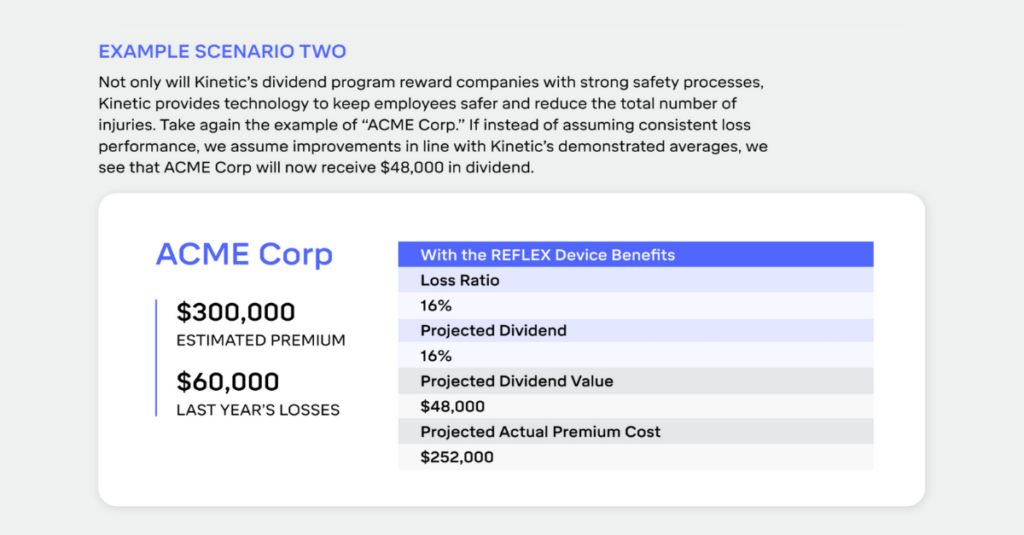

Example Scenario Two

Not only will Kinetic’s dividend program reward companies with strong safety processes, Kinetic provides technology to keep employees safer and reduce the total number of injuries. Take, again, the example of “ACME Corp.” If instead of assuming consistent loss performance, we assume improvements in line with Kinetic’s demonstrated averages, we see that ACME Corp will now receive $48,000 in dividends.

Contact us today to learn more about the Kinetic Insurance Workers’ Compensation Dividend Plan.